The Bridge Between Your Crypto and Your Naira Life

How Busha's SOL-Backed Loans Work

Nigerian crypto holders exist between two financial systems that don’t communicate. One is where your wealth lives: Solana, Bitcoin, USDT, dollar-denominated assets that hold value while the naira loses purchasing power year after year. The other is where your life happens — rent, bills, business expenses, school fees — everything that keeps your world running requires naira in your bank account.

For as long as you’ve held crypto, the only bridge between these systems has been to sell. Need cash? Convert your position, absorb whatever the P2P rate is that day, and exit your holdings. You solve today’s problem, but give up tomorrow’s upside. Sell your SOL to handle an emergency, watch it rally next month — you didn’t just pay for the emergency, you paid for it twice.

Busha’s Solana-backed loans solve this. You can now borrow naira using your SOL as collateral. Your crypto stays in your wallet — no exit, no permanent conversion. The cash you need appears in minutes. You repay when you’re ready, your collateral unlocks, and any appreciation that happened while your SOL sat as collateral — you get to keep.

This isn’t a convenient feature. It’s a bridge between two systems that weren’t built to work together, finally working together.

Here’s exactly how it works.

From Collateral to Cash

Accessing a Solana-backed loan on Busha isn’t as complicated as you’d think. Traditional bank loans come with a hundred and one steps. Busha’s process—depositing collateral, taking out the loan, monitoring your position, repaying—is seamless.

Here’s how each step works from start to finish.

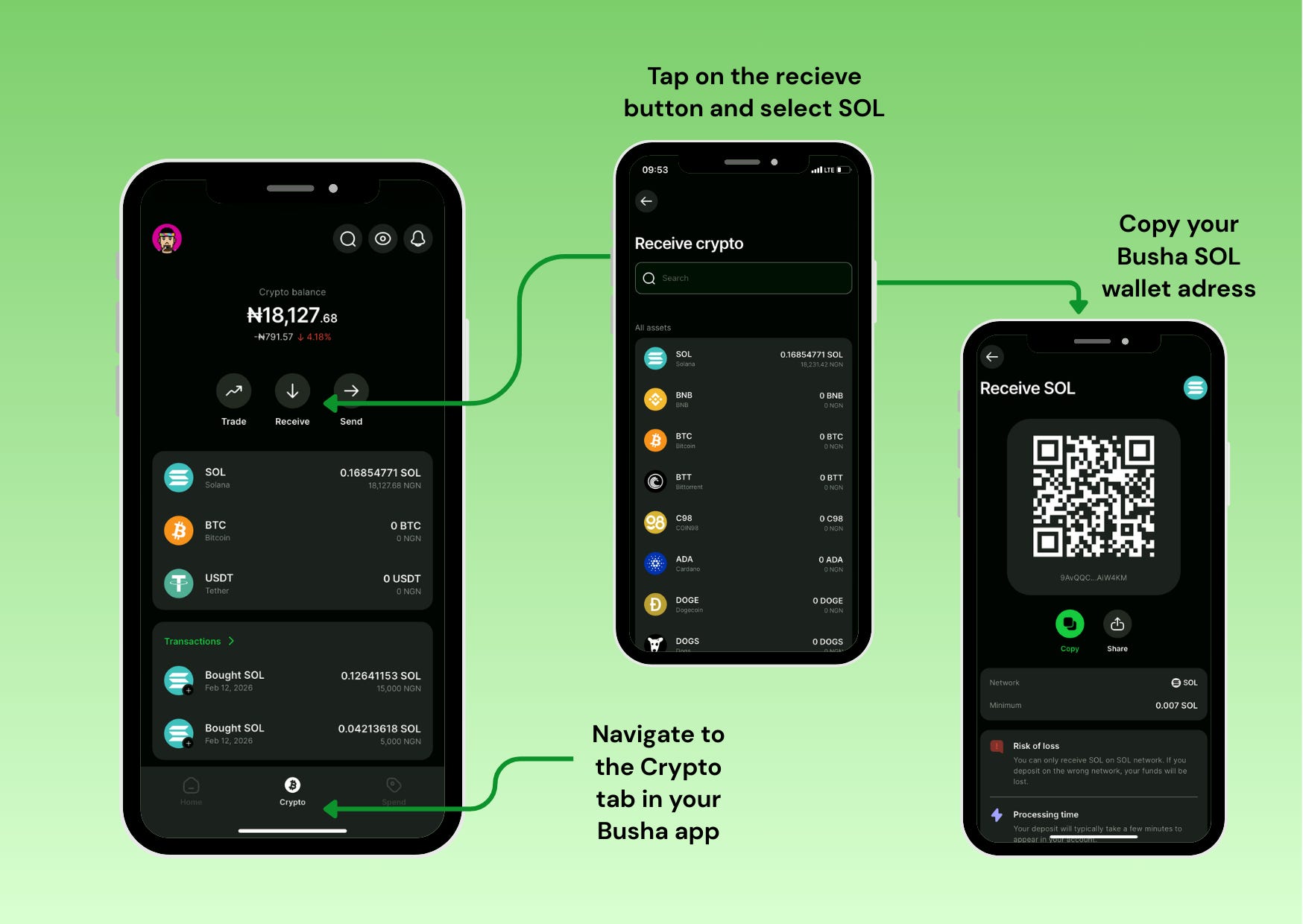

Depositing Collateral

Before you can borrow, you need SOL in your Busha crypto wallet. If you already have SOL on Busha, skip to the next section. If you’re depositing from an external wallet or exchange, follow these steps.

Open your Busha app and navigate to the Crypto tab, tap “Receive”

Select SOL from the list of available assets.

You’ll see your Busha SOL wallet address displayed as both a QR code and a text string. You can share this address or copy it to send SOL from another wallet or exchange.

Once the SOL arrives in your Busha wallet, the amount appears in your crypto balance. This is your collateral. The more SOL you hold, the more you can borrow.

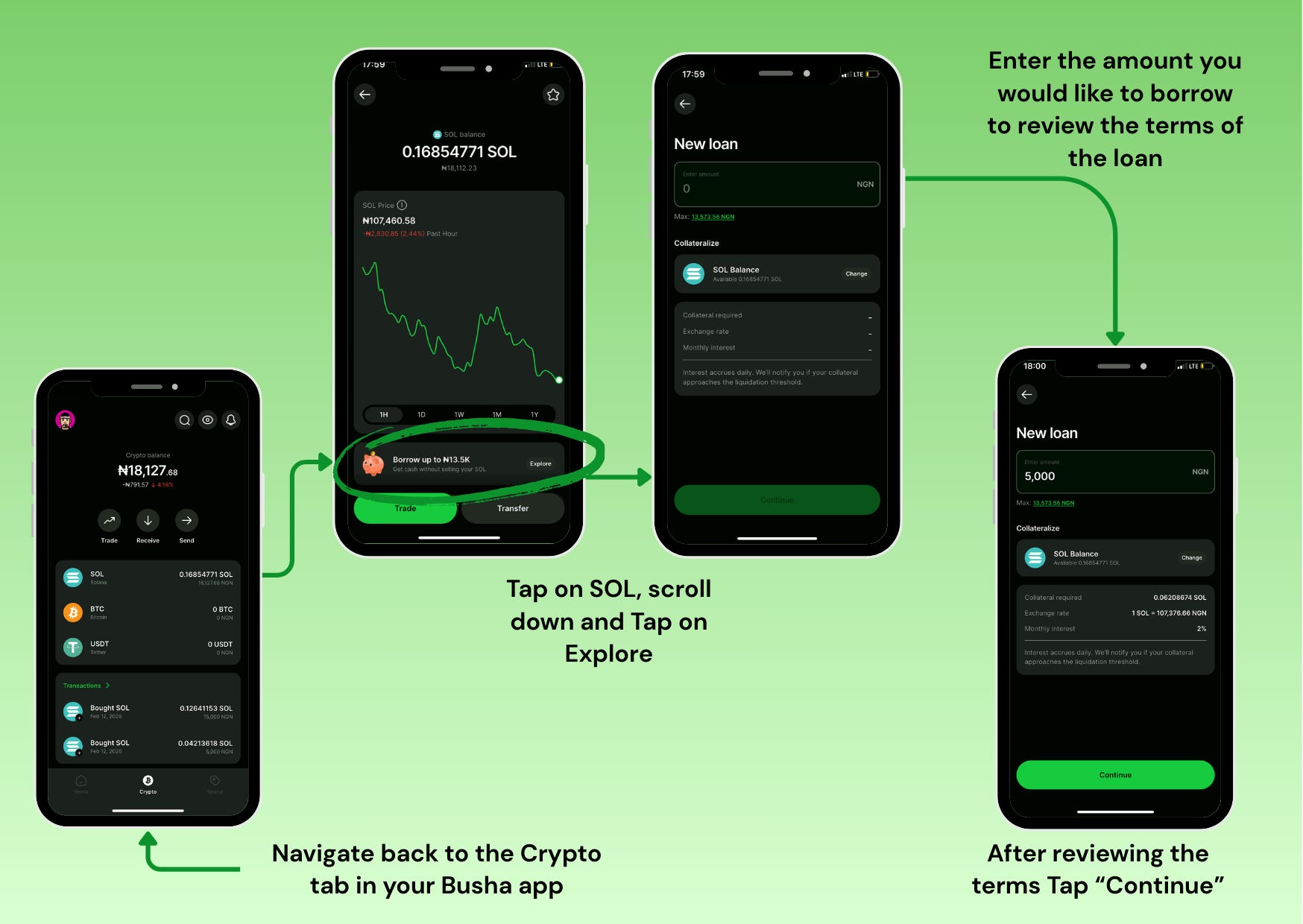

Taking Out your Loan

With SOL in your wallet, you’re ready to borrow. The process from seeing your loan offer to receiving naira takes just a few taps.

Navigate back to the Crypto tab in your app, tap on your SOL holdings to see the detail view. Scroll down, and a banner will show your maximum borrowing capacity:

“Borrow up to ₦13.5K - Get cash without selling your SOL.”

Tap “Explore”

The loan interface will appear. Enter the amount you need within your maximum borrowing capacity—₦5,000 is used for this example.

The system calculates instantly, showing three things:

How much SOL gets locked as collateral (0.062 SOL)

The current exchange rate (1 SOL = ₦107,376),

The monthly interest on your loan (2%).

Monthly interest is what you pay to borrow. At 2% per month on ₦5,000, that’s ₦100 monthly. Hold the loan for 10 days, you pay about ₦33. Hold it for three months, you pay ₦300 total. The interest accrues daily, so you only pay for the exact time you use the money.

Tap “Continue”

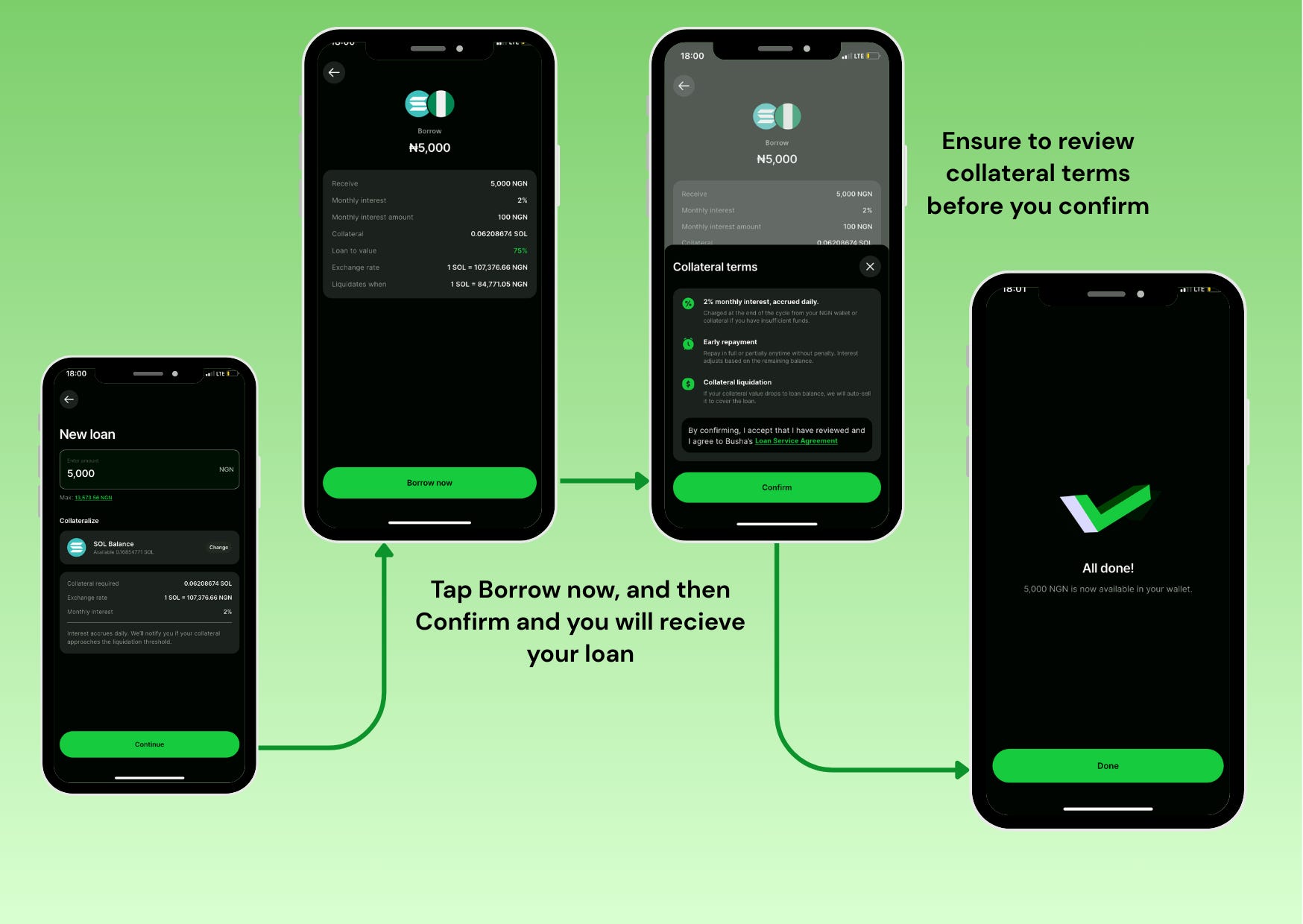

The confirmation screen will pop up and will show you every detail you need to know before finalizing the loan:

What you receive: ₦5,000

Monthly interest amount: ₦100

Collateral locked: 0.062 SOL

Loan-to-value ratio: 75%

Liquidation threshold: ₦84,771 per SOL

What you need to pay the most attention to is your Loan-to-value ratio and Liquidation threshold, as they ensure that your Loan is healthy and you don’t default on it due to Solana’s price action.

Loan-to-value (LTV) is the relationship between what you're borrowing and what your collateral is worth. At 75% LTV, you're borrowing ₦75 for every ₦100 of SOL value you lock up. In our example, the 0.062 SOL collateral is worth ₦6,666, and you're borrowing ₦5,000 against it. The difference—₦1,666—is your safety buffer against price movement.

Liquidation threshold is the price level where action is needed. In our illustration SOL currently sits at ₦107,376. "If SOL drops to ₦84,771—a 21% decline from the current price—your safety buffer is gone and you risk liquidation.

Before that happens, you’ll receive alerts from Busha asking you to either add more SOL as collateral or pay down part of the loan. Liquidation only happens if you ignore these warnings and SOL continues dropping in price.

The collateral terms modal appears before final confirmation. Three key terms:

2% monthly interest, accrued daily: Interest compounds every day and is charged when you repay the loan. Busha deducts from your naira wallet first. If you don't have enough naira, it converts a small portion of your collateral to cover the interest.

Early Repayment: You can repay in full or in part at any time without penalty. Interest adjusts based on your remaining balance. Borrowed for what you thought would be three months, but got paid early? Repay after two weeks and only pay interest for those two weeks.

Collateral liquidation: If your collateral value drops to equal your loan balance, Busha will automatically sell it to cover the loan. This protects both you and Busha from your debt exceeding your collateral value. Remember: you will get multiple warnings well before this point.

Review the terms and tap “Confirm”

Success. “5,000 NGN is now available in your wallet.”

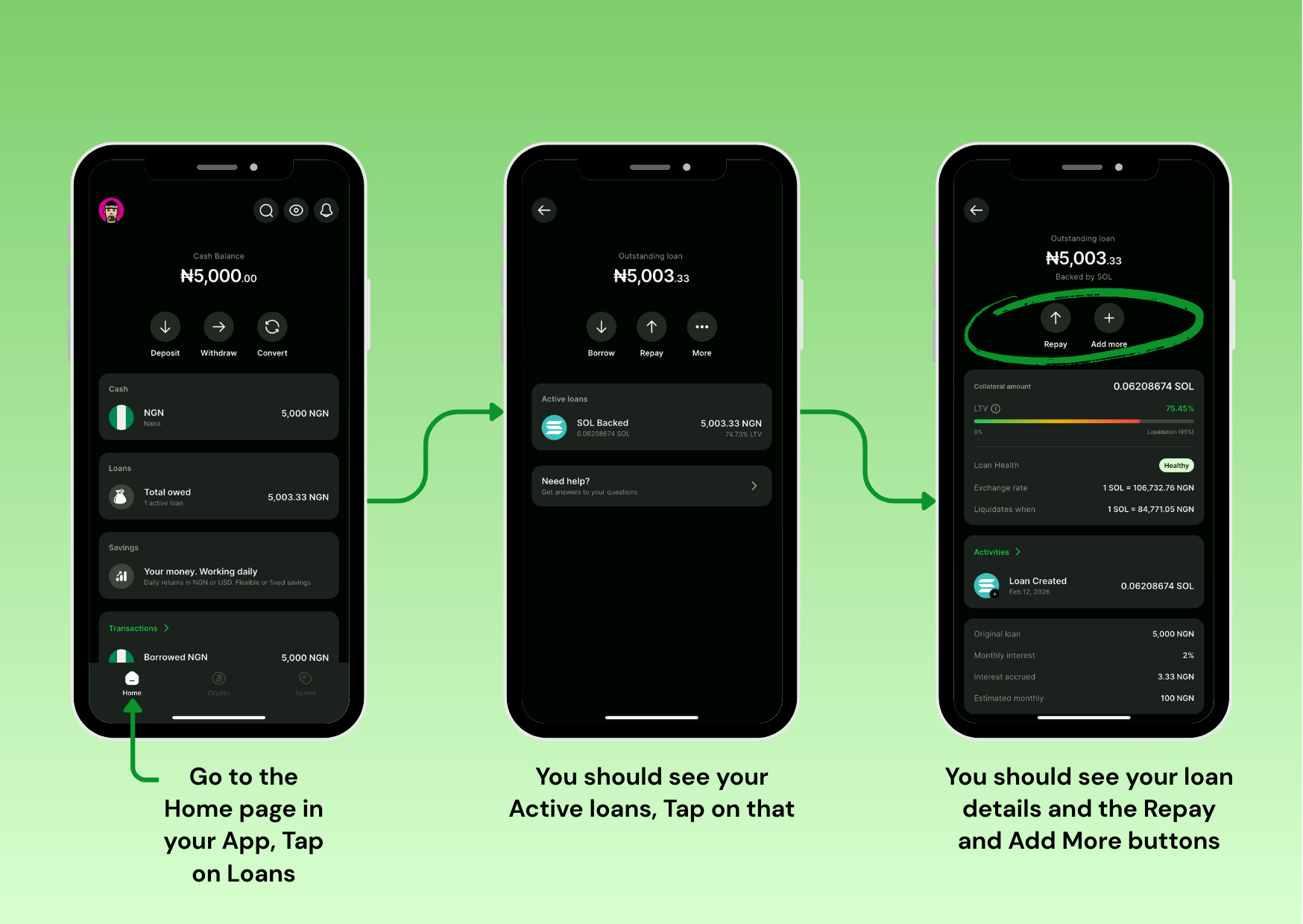

Monitoring Your Loan

Once your loan is active, you can monitor it anytime from your Busha app. The interface gives you complete visibility into your loan health, outstanding balance, and options to manage your position.

To monitor your Loan navigate to the Home tab in your app.

Under “Loans,” you’ll see “Total owed” with your current balance (₦5,003.33 in this illustration) and “1 active loan.” Tap on this section.

The Loans Overview screen will appear, displaying your outstanding loan amount (₦5,003.33) at the top, along with three action buttons: Borrow, Repay, and More.

Under “Active loans,” you’ll see your SOL-backed loan with the amount owed (₦5,003.33), collateral locked (0.062 SOL), and current LTV percentage (74.73%).

Tap on the active loan to see full details.

The loan detail screen shows everything you need to monitor your position:

At the top, your outstanding loan amount (₦5,003.33) is backed by SOL, with two action buttons: Repay and Add more.

Repay lets you pay down your loan partially or in full.

Add more lets you borrow additional naira if your collateral can support it.

Below that, your key metrics:

Collateral amount: 0.06208674 SOL—the exact amount locked in your loan.

LTV bar: A visual indicator showing your loan-to-value ratio at 75.45%. The bar runs from green (safe) through yellow (caution) to red (liquidation risk at 95%). Your current position sits in the green zone.

Loan Health: Healthy—a quick status indicator. This badge turns yellow or red as your LTV approaches risky levels.

Exchange rate: 1 SOL = ₦106,732.76—the current market price of SOL. This updates in real-time and directly affects your LTV.

Liquidates when: 1 SOL = ₦84,771.05—the critical threshold. If SOL drops to this price, you’ll need to take action or face liquidation.

Notice the exchange rate has changed slightly since the loan was created (from ₦107,376 to ₦106,732). This small drop caused the LTV to move from 75% to 75.45%. You’re still firmly in healthy territory, but you can see how price movement affects your position in real-time.

Below the metrics, the Activities section shows your loan timeline—when it was created and how much collateral was locked.

At the bottom, your loan summary:

Original loan: 5,000 NGN

Monthly interest: 2%

Interest accrued: 3.33 NGN

Estimated monthly: 100 NGN

The “Interest accrued” increments daily. In this example, ₦3.33 has accrued since the loan was created. The “Estimated monthly” shows what you’d pay in interest if you held the loan for a full month.

This dashboard updates automatically as SOL’s price moves and interest accrues. Check it anytime to see exactly where you stand.

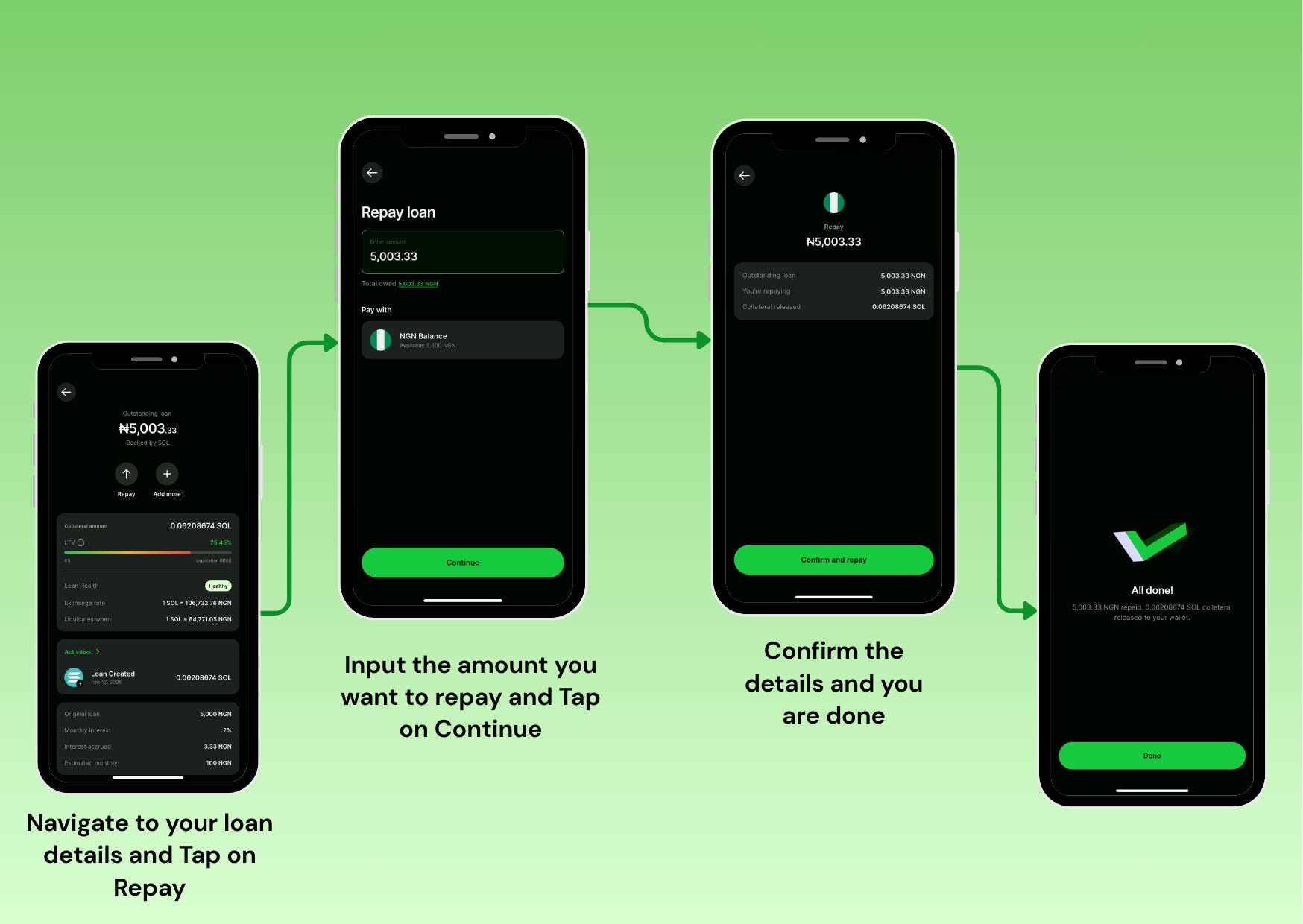

Repaying Your Loan

When you’re ready to close your loan, the repayment process is straightforward. You can repay in full or pay down a portion of your balance—there are no penalties for early repayment.

From your loan detail screen, tap the Repay button at the top.

The repayment screen appears with your total owed amount pre-filled: ₦5,003.33 in this example. Below it shows “Total owed: 5,003.33 NGN” in green to confirm the amount.

Under “Pay with,” you’ll see your NGN Balance with available funds (₦5,600 in this example). You can repay the full amount shown or edit the field to make a partial payment.

Tap “Continue.”

The confirmation screen shows exactly what’s happening:

Repay: ₦5,003.33

Outstanding loan: 5,003.33 NGN

You’re repaying: 5,003.33 NGN

Collateral released: 0.06208674 SOL

This makes it clear—you’re paying the full balance and all your collateral unlocks immediately.

Tap “Confirm and repay”

Success. “All done! 5,003.33 NGN repaid. 0.06208674 SOL collateral released to your wallet.”

Your SOL is back in your trading wallet. The loan is closed. In this example, the loan lasted one day with a total interest of ₦3.33.

Now you understand how SOL-backed loans work on Busha—from deposit to repayment. The real question is: when does borrowing against your SOL make more sense than selling it?

When Borrowing Beats Selling

Now you understand how SOL-backed loans work on Busha, from deposit to repayment. But knowing how it works and knowing when to use it are different things. The pattern is consistent, though whenever real money is on the line, and selling means giving up upside you believe in, borrowing changes the math. Your SOL stops being an asset you can’t touch without selling and starts functioning as borrowing capacity, instantly verifiable, globally liquid, transparently valued. Here’s what that looks like in practice.

Emergency Cash Access

Your check engine light has been blinking for a week. You finally take it to the mechanic, and the verdict comes back: transmission repair, ₦400,000. Not optional — the car doesn’t move without it. You need it for work, and every day without it costs you money.

You have the funds. Over the past year, you’ve been stacking SOL with 30% of every paycheck from your remote tech job — 8 SOL now worth ₦880,000 at ₦110,000 per coin. You’ve watched it climb from ₦80,000, and everything your conviction tells you is that this rally isn’t done.

You could sell 3.6 SOL, fix the car, and move on. But selling means exiting a chunk of your position right when the momentum is building.

You deposit your 8 SOL into your Busha wallet. Your maximum loan capacity shows up: ₦660,000. You borrow ₦400,000. The mechanic gets paid. Your full 8 SOL position stays intact.

Three months later, SOL hits ₦140,000. Your 8 SOL is now worth ₦1,120,000 — it appreciated by ₦240,000 while locked as collateral. You repay your loan: ₦424,000 total (₦400,000 principal + ₦24,000 interest). After interest, you’re ₦216,000 ahead of where you’d be if you’d sold and missed that appreciation.

The car is fixed. The position is whole. The rally wasn’t missed.

Business Opportunity

Inventory moves fast in your Lagos retail business, but capital is always tight. You’ve been disciplined — converting parts of your profits into crypto instead of letting naira sit and lose value. You now hold 30 SOL worth ₦3.3 million at ₦110,000 per SOL.

Your supplier calls on a Tuesday morning. They’re overstocked and need to move product: 20% off bulk inventory if you pay cash by Friday. The discount saves you ₦800,000, but you need ₦2 million upfront. You didn’t plan for this. You could sell 18 SOL to raise the cash, but that means exiting most of your position at ₦110,000 with no guarantee you can buy back at that price when cash flow returns.

You deposit your 30 SOL into your Busha wallet and borrow ₦2 million. You call your supplier back and confirm the order. Your SOL position stays locked as collateral.

One month later, SOL rallies 20% to ₦132,000. Your 30 SOL is now worth ₦3.96 million — it appreciated by ₦660,000 while you held it. You repay your loan from sales revenue: ₦2,040,000 total (₦2M principal + ₦40,000 interest). You captured both the business opportunity and the SOL rally, coming out ₦620,000 ahead after interest.

Riding Out a Dip

You’re a freelance designer who’s been converting a portion of every client payment into SOL for the past year. You now hold 12 SOL worth ₦1.32 million at ₦110,000 per coin. Last month, you borrowed ₦400,000 against your SOL to cover a deposit on new equipment for your studio.

Then the market corrects. SOL drops 18% over two weeks to ₦90,000. Your LTV climbs from 75% toward the caution zone. Busha sends you an alert.

If you’d sold SOL to fund that equipment deposit, this dip wouldn’t matter — but you also wouldn’t have those coins anymore. Instead, you still hold your full position, and you have options. You transfer 2 additional SOL from an external wallet into your Busha account and add them as collateral. Your LTV drops back into the green. No panic. No liquidation. No forced sale at the worst possible price.

Six weeks later, SOL recovers to ₦120,000. Your 14 SOL is now worth ₦1.68 million. You repay your loan — ₦416,000 total with interest — and your collateral unlocks. You rode out the dip with your position intact and came out the other side with more value than you started with.

The loan didn’t just give you liquidity. It gave you time — and in crypto, time in the market is everything.

Each of those scenarios is different, but they share something fundamental: the ability to access naira without dismantling a crypto position. For anyone holding SOL in Nigeria, that changes what the asset actually is.

Why Solana

Busha didn’t build this around Solana by accident. Of all the networks Nigerian crypto holders use actively, Solana has carved out a specific role, and it’s not just as a token people buy and hold.

Nigerians are deep in the Solana ecosystem. They trade on Solana DEXs, participate in DeFi protocols, mint and trade NFTs on Solana marketplaces, and use SOL for cross-border transfers. The network isn’t theoretical here; it’s the infrastructure people interact with daily. Busha building lending around SOL means it’s building around an asset its users already hold and a network they already live on.

Then there’s the asset itself. SOL isn’t a stablecoin — it’s a growth asset, and that’s exactly why holders are reluctant to sell it. If you bought SOL at ₦30,000 and watched it climb to ₦110,000, every naira you convert out of that position feels like leaving money on the table. The stronger your conviction about where SOL is heading, the more painful selling becomes. That’s the exact psychology that makes collateral-backed borrowing valuable — it lets you stay positioned in an asset you believe has significant upside left.

And Solana’s speed makes the lending experience actually work. Transactions settle in seconds, not minutes or hours. When Busha says you can go from collateral deposit to naira in your wallet in under three minutes, that’s only possible because the underlying network moves at that pace. A lending product built on a slower chain would mean longer waits, more friction, and a user experience that feels closer to traditional banking than it should.

This is what crypto maturing beyond speculation looks like. Not just price appreciation, but practical utility — holders deploying their assets without dismantling them.

Closing

For years, accessing naira liquidity meant dismantling your crypto position. You handled today’s expense by giving up tomorrow’s appreciation. That wasn’t a flaw in crypto — it was a missing piece of infrastructure.

Busha’s SOL-backed loans fill that gap. Think about the last time you sold crypto to cover something urgent. The rate you absorbed. The position you exited. The rally you watched happen without you. Now imagine that same situation, but instead of selling, you borrow against your SOL, handle what needs handling, and repay when you’re ready — with your full position intact and every bit of appreciation still yours.

That option exists now. If you hold SOL on Busha, you can access it today. If you don’t have Busha yet, download the app, fund your wallet, and the next time life demands naira, your crypto doesn’t have to be the casualty.

Busha’s SOL-backed loans represent a shift from crypto as something you hold and hope to crypto as something you hold and use. Your wealth and your daily financial life no longer have to exist in separate worlds.

The bridge has been built. And it works in both directions.